2016 Year in Review: The Bagel Family's Annual Spending Report

My goal for the last few years has been to keep our household spending under $40,000 (that is to say, spending out of our net paychecks: this doesn't included taxes and other paycheck deductions, nor does it include savings.) This year, I massively failed. Right now, we're coming in at about $65,000 with maybe another $5,000 in projected expenses for the month of December.

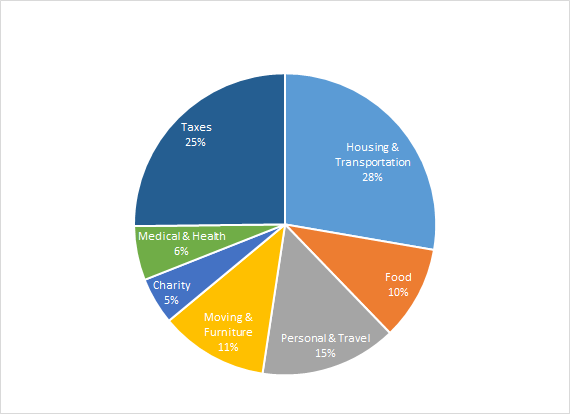

Here's how it (roughly) breaks down, including projected December expenses. This is for both my wife and me.

Avg. $2250/mo

This includes mortgage/condo fees/property tax from when we lived in a condo, rent (including as yet unpaid December rent), utilities, insurance, etc. We live in an expensive city, and our rent is higher than our mortgage was, so I'm not sure $40,000 is really realistic now that we're renting. Now, it's kind of disingenuous to be beating myself up about this without taking into account the gains we realized when we sold the condo. But that's what I'm doing!

Transportation: $500

Avg. $42/mo

Given my impassioned plea to consider housing and transportation costs together, our light transit costs should hopefully balance our heavy housing costs (a bit). As of July, our commute costs are nil, since my wife works from home and I got a rail pass from work.

Food: $10,000

Avg. $833/mo

$5,500 of this is groceries, Our grocery costs definitely went up at our new apartment. We no longer live near a grocery store, so we've been getting Instacart routinely. About $3,000 of this is my wife and I eating out together (dinner dates, brunch with friends, ordering pizza, etc.) The remaining $1,500 is me getting lunch and coffee out almost every day.

My Personal Spending: $6,500

Avg. $541/mo

This is the category I usually break down in my monthly reviews/one year purchase reviews. There's a lot of miscellany in here, but major subcategories include hobbies ($900), which includes fitness clothes and art supplies; work clothes ($550); and casual clothes ($500).

Wife's Personal Spending: $6,000

Avg. $500/mo

This is not as big as a disparity as I thought it would be… but note that I don't itemize my wife's free spending, so this figure includes all her personal eating out/coffee/drinks with friends/etc, whereas mine is reported in Food above. So really, my free spend was more like $8,000 to her $6,000.

This includes things we wouldn't have had to pay if we hadn't moved: up-front rental fees, the move itself. Some of this will be returned to us (security deposit, etc.), but not until next year. I can't say we won't have these expenses next year, as our lease is for one year so we might have to move again. But we should be able to put our returned deposits toward those fees.

Home Furnishings: $4,500

We usually spend some amount on home furnishings, but nowhere near this. I think we replaced nearly every item of furniture we own around the move.

Travel: $2,000

Most of this is family-related travel. $750 is airfare for an upcoming non-family vacation we haven't taken yet (and doesn't account for the full cost of that trip.)

Charity: $5,000

This is one area where I hope to do more before the year is out!

Medical - $1,200

Avg. $100/mo

We pay for most medical expenses through our FSA.

Health insurance - $4,550

Avg. $379/mo

Taxes - $25,000

This is definitely a rough projection. I won't really know until I do our taxes. This is assuming our withholding is more or less correct, but a lot of tax stuff has changed this year (income, savings, property ownership) so I really don't know.

Total Invisible Expenses: $30,750

That said, taxes scale with income, so we don't have to worry too much about that in a retirement/pay cut situation. (That's why I usually don't bother calculating taxes as outgoings when I evaluate how frugal I'm being.)

So, for everything else, what can we do differently next year?

I don't anticipate being able to reduce housing much as long as we stay in the same city/housing market. We'll either stay in the same place or go somewhere with equivalent rent. Given that, $50,000 may be a more realistic goal than $40,000.

But we should be able to keep moving-related and home goods down even if we move within town. This year's move was our first after a long period of living in the same place, so we took the opportunity to replace a bunch of stuff, and we were also not as savvy as I think we could have been. Hopefully, if I look back in the same way next year, these expenses will be very different. This accounts for over $10,000 this year, so getting rid of them would make a huge difference.

I don't have big problems with travel, charity, or medical.

Food and personal spending jump out as the ongoing categories with the greatest scope for cutting the fat, but they've also proved the most resistant to change. Because I love them! I LOVE FOOD. Each savings dollar is going to hard-won here.

Here's how it (roughly) breaks down, including projected December expenses. This is for both my wife and me.

Regular Expenses

Housing: $27,000Avg. $2250/mo

This includes mortgage/condo fees/property tax from when we lived in a condo, rent (including as yet unpaid December rent), utilities, insurance, etc. We live in an expensive city, and our rent is higher than our mortgage was, so I'm not sure $40,000 is really realistic now that we're renting. Now, it's kind of disingenuous to be beating myself up about this without taking into account the gains we realized when we sold the condo. But that's what I'm doing!

Transportation: $500

Avg. $42/mo

Given my impassioned plea to consider housing and transportation costs together, our light transit costs should hopefully balance our heavy housing costs (a bit). As of July, our commute costs are nil, since my wife works from home and I got a rail pass from work.

Food: $10,000

Avg. $833/mo

$5,500 of this is groceries, Our grocery costs definitely went up at our new apartment. We no longer live near a grocery store, so we've been getting Instacart routinely. About $3,000 of this is my wife and I eating out together (dinner dates, brunch with friends, ordering pizza, etc.) The remaining $1,500 is me getting lunch and coffee out almost every day.

My Personal Spending: $6,500

Avg. $541/mo

This is the category I usually break down in my monthly reviews/one year purchase reviews. There's a lot of miscellany in here, but major subcategories include hobbies ($900), which includes fitness clothes and art supplies; work clothes ($550); and casual clothes ($500).

Wife's Personal Spending: $6,000

Avg. $500/mo

This is not as big as a disparity as I thought it would be… but note that I don't itemize my wife's free spending, so this figure includes all her personal eating out/coffee/drinks with friends/etc, whereas mine is reported in Food above. So really, my free spend was more like $8,000 to her $6,000.

Irregular Expenses

Moving-related: $7,000This includes things we wouldn't have had to pay if we hadn't moved: up-front rental fees, the move itself. Some of this will be returned to us (security deposit, etc.), but not until next year. I can't say we won't have these expenses next year, as our lease is for one year so we might have to move again. But we should be able to put our returned deposits toward those fees.

Home Furnishings: $4,500

We usually spend some amount on home furnishings, but nowhere near this. I think we replaced nearly every item of furniture we own around the move.

Travel: $2,000

Most of this is family-related travel. $750 is airfare for an upcoming non-family vacation we haven't taken yet (and doesn't account for the full cost of that trip.)

Charity: $5,000

This is one area where I hope to do more before the year is out!

Invisible Expenses

These are expenses that are taken out of our paycheck before we see it; things I didn't include in my $70,000 projection and wouldn't ordinarily include in my $40,000 per year goal, but which nonetheless affect our financial state. I'm calculating this mostly out of curiosity!Medical - $1,200

Avg. $100/mo

We pay for most medical expenses through our FSA.

Health insurance - $4,550

Avg. $379/mo

Taxes - $25,000

This is definitely a rough projection. I won't really know until I do our taxes. This is assuming our withholding is more or less correct, but a lot of tax stuff has changed this year (income, savings, property ownership) so I really don't know.

Total Invisible Expenses: $30,750

Next Steps

Sooo…. It's kind of upsetting that our total outgoings are about $100,000 year! Definitely not frugal. We have to make so much to maintain that standard of living!That said, taxes scale with income, so we don't have to worry too much about that in a retirement/pay cut situation. (That's why I usually don't bother calculating taxes as outgoings when I evaluate how frugal I'm being.)

So, for everything else, what can we do differently next year?

I don't anticipate being able to reduce housing much as long as we stay in the same city/housing market. We'll either stay in the same place or go somewhere with equivalent rent. Given that, $50,000 may be a more realistic goal than $40,000.

But we should be able to keep moving-related and home goods down even if we move within town. This year's move was our first after a long period of living in the same place, so we took the opportunity to replace a bunch of stuff, and we were also not as savvy as I think we could have been. Hopefully, if I look back in the same way next year, these expenses will be very different. This accounts for over $10,000 this year, so getting rid of them would make a huge difference.

I don't have big problems with travel, charity, or medical.

Food and personal spending jump out as the ongoing categories with the greatest scope for cutting the fat, but they've also proved the most resistant to change. Because I love them! I LOVE FOOD. Each savings dollar is going to hard-won here.

Comments

Post a Comment